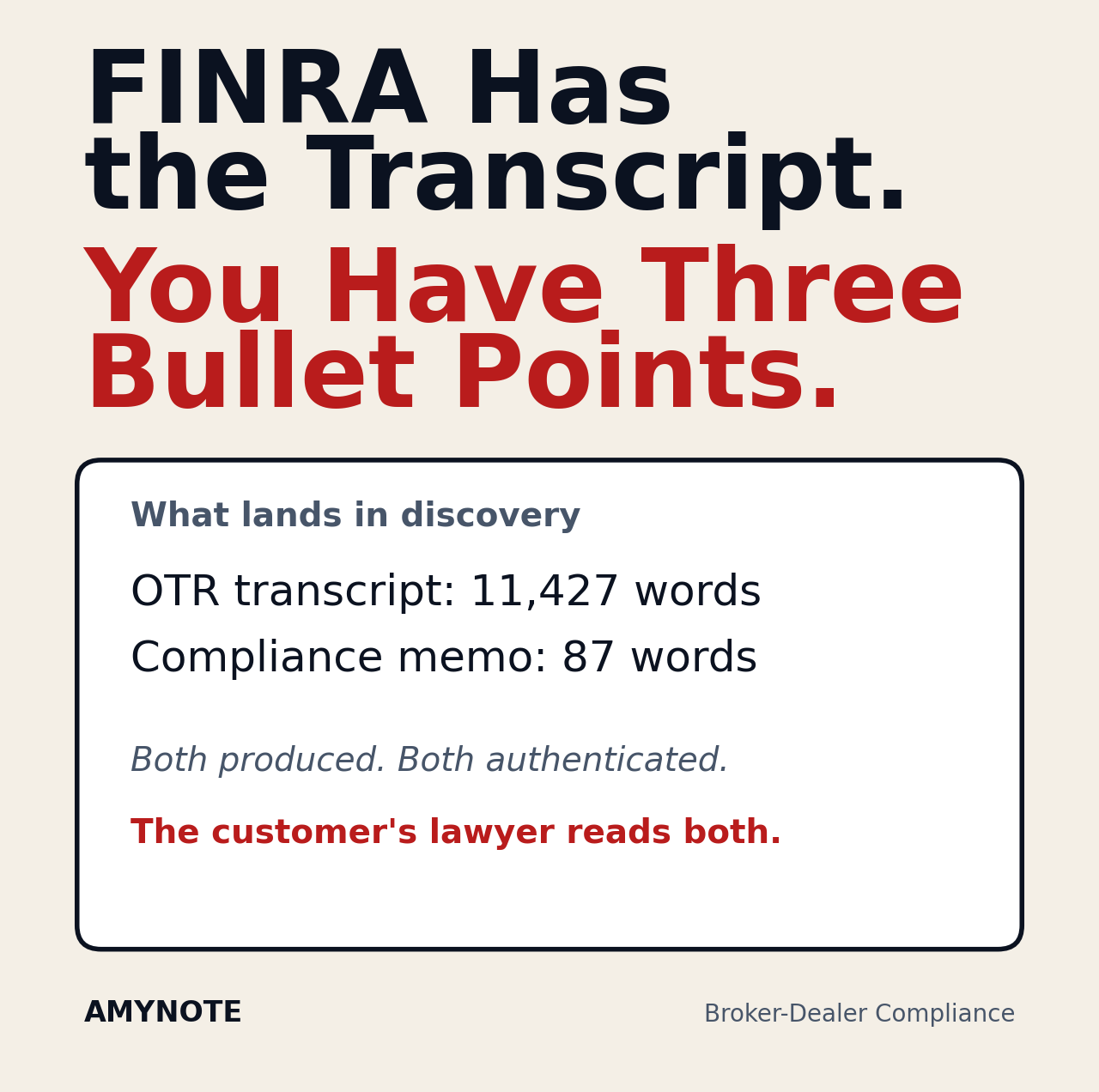

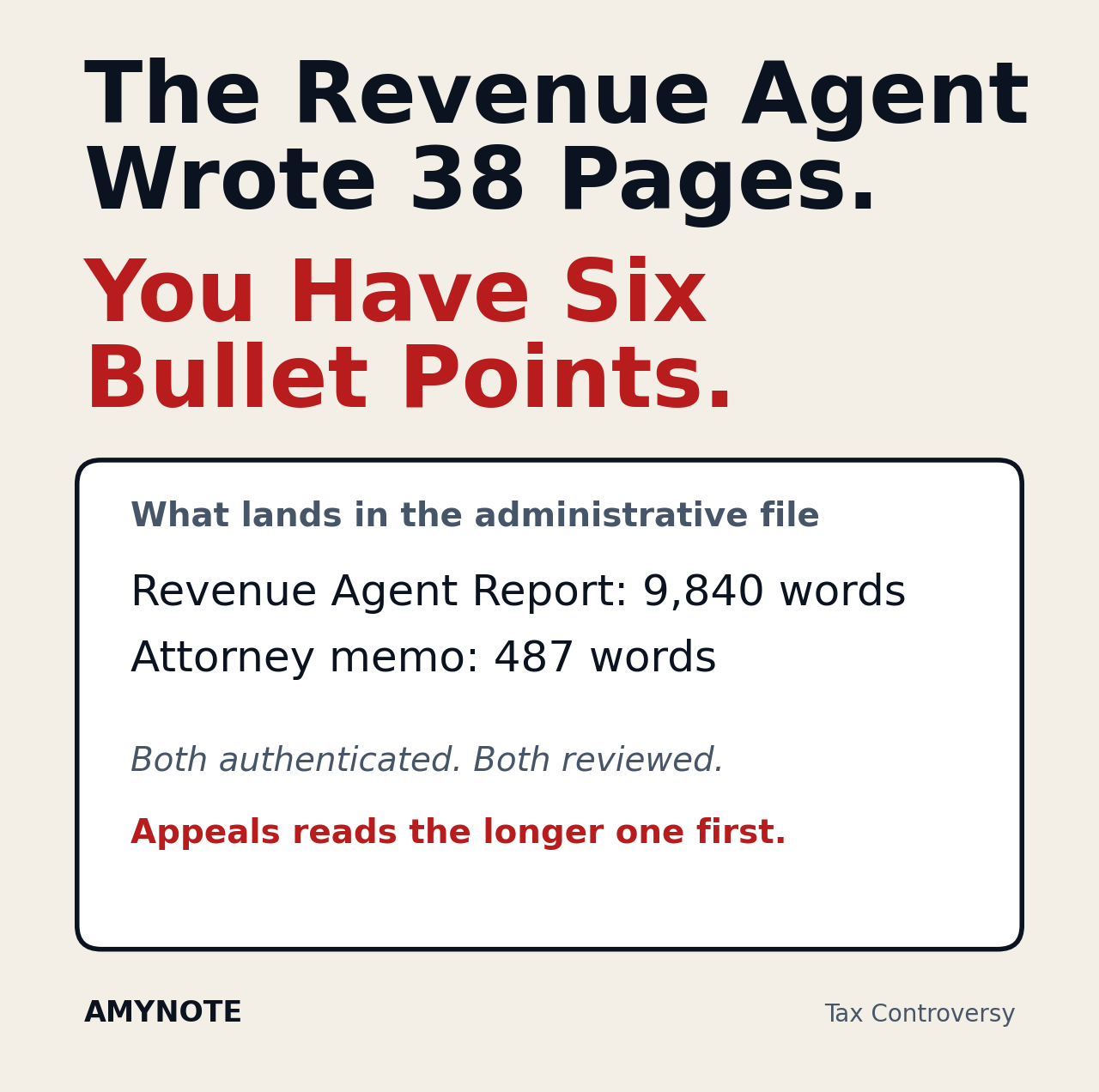

The Revenue Agent's notebook fills up. Yours does not. Six months later, the Revenue Agent Report lands on your desk and reads like a different meeting. The taxpayer remembers the conversation one way. The Report describes it another. Your notes are too thin to settle the argument.

That gap is not a clerical problem. It is the structural problem of IRS controversy practice: the side with the verbatim record controls the factual narrative, and the verbatim record almost always belongs to the IRS.

The Problem

The IRS field audit interview is a fact-finding exercise where one side keeps score. The Revenue Agent arrives with Form 4564 information requests, asks structured questions, and writes everything down. Workpapers, lead sheets, and contemporaneous notes feed directly into the Revenue Agent Report. By the end of the exam, the agent's file is dozens of pages of dated, time-stamped, sourced narrative.

You walk out with three pages of handwritten bullets. Your client paraphrases what they "think" was asked. Six weeks later, the 30-day letter arrives with proposed adjustments resting on statements you do not remember the client making. You file a protest. The Appeals Officer reads the Revenue Agent Report first because it is the longer, more detailed document in the file. Your client's recollection has already drifted.

By the time you reach Appeals, the factual record belongs to the IRS by default. By the time you reach Tax Court, the Revenue Agent Report has been cited, quoted, and treated as the contemporaneous account of what was said. Your three pages of bullets cannot rebut it. They were never intended to.

Why the Asymmetry Matters

An IRS audit is not a court proceeding, but its factual record gets used like one. The Revenue Agent Report informs:

- The 30-day letter and proposed adjustments. The agent's interpretation of what the taxpayer said is baked into the deficiency notice from day one.

- The Appeals Officer's hazards-of-litigation analysis. Appeals weighs the case based on the record as written, not the record as remembered.

- Subsequent Tax Court or refund litigation. The agent's notes are admissible. The taxpayer's lawyer's memo, usually, is not the kind of document a judge will lean on.

- Penalty determinations. Substantial understatement and accuracy-related penalties often turn on whether the taxpayer "knew" something at a particular point in time. The agent's note that says "taxpayer stated he was aware of" is treated as evidence of that knowledge.

The taxpayer cannot afford to enter Appeals or Tax Court with a thinner version of the facts than the IRS has. The Service's record is going to be the longer document. Without a verbatim record of your own, you are litigating the agent's narrative, not your own.

Why Current Solutions Fail

Most practitioners try one of three workarounds. Each has a structural reason it does not close the gap.

- Dictating notes into a recorder after the meeting. Memory degrades within hours. By the end of a four-hour exam, the dictation captures impressions, not exchanges. A specific question and a specific answer become "we discussed depreciation methods." The wording the agent used — the wording that will appear in the Report — is gone.

- Having a paralegal sit in and take notes. Typing speed caps coverage at roughly 60 percent of spoken content, and the paralegal cannot caucus with the attorney without missing what the agent says next. The result is selective notes that look complete until the Report quotes a question your notes never recorded.

- Requesting the agent's own notes through a FOIA request. Those notes arrive heavily redacted, months later, and only after the factual narrative has already hardened in Appeals. They are useful for a Tax Court trial, not for the protest that needed them.

The deeper issue is that none of these methods produce a record on the same scale as the agent's. Six bullet points cannot rebut a 38-page narrative, regardless of how careful the bullets are.

What Actually Works

The fix is having your own verbatim record of the interview, taken in real time and searchable on the way out the door. IRC Section 7521(a)(1) expressly permits the taxpayer to make an audio recording of any in-person interview with the IRS, provided the taxpayer gives the agent ten calendar days' advance written notice. The statute has been on the books since 1988. Most practitioners never invoke it because the postprocessing burden of a four-hour audio file is worse than the original problem — the recording exists, but it is unsearchable until somebody pays a court reporter or types it out.

An AI-assisted record changes that calculation. The marginal cost of producing a searchable, speaker-labeled transcript of the interview has dropped to near zero. The Revenue Agent Report is still going to be 38 pages. Now your record is too — and yours has the exact words the agent used, not the agent's paraphrase of what the taxpayer said.

Where AmyNote Fits

AmyNote runs on the attorney's phone during the interview, transcribes in real time using OpenAI's Whisper-class Speech API, and uses Anthropic's Claude Opus for speaker diarization and structured summaries. By the time you reach the parking lot, the transcript is searchable with speaker labels and timestamps. Both OpenAI and Anthropic contractually guarantee zero training on user data. Audio is encrypted in transit; processing copies may be retained to deliver and recover requested features. Transcripts are stored locally on the attorney's device with encrypted transport.

When the Revenue Agent Report lands, you open the transcript and search the agent's exact words against the Report. Where the Report says "the taxpayer admitted," the transcript shows the actual question and the actual answer. Where the Report cites a "concession," the transcript shows whether anyone in the room used that word. That is a protest letter that writes itself.

The same record reshapes Appeals. The hazards-of-litigation conversation changes when you can point to a specific exchange and say, "the Report characterizes this as a concession; here are the actual words." Appeals Officers respond to verbatim records. They do not respond to "we recall it differently."

Getting Started

Send the ten-day Section 7521 notice the moment the audit appointment is set. Write it in plain language: "Pursuant to IRC Section 7521(a)(1), the taxpayer will make an audio recording of the in-person interview scheduled for [date]." Bring a second device as a backup. If the client is sensitive about cloud transit, run AmyNote in airplane mode and sync afterward — the on-device transcription works without a network connection.

The point is not to win the audit at intake. The point is that when Appeals or Tax Court asks what was actually said, you can answer with the same precision the Revenue Agent did. Your file has 38 pages too. They say what actually happened.

Originally published as an X Article.